Boeing.

A moatless company – even though it has a dominant position.

Moat Score analysis showing a weak 2.8 out of 10 rating based on NabzdykRatings proprietary algorithm.")

Boeing has a Nabzdyk Ratings moat score of 2.8/10. The company is barely profitable, and its “switching cost” in terms of creating a service-based revenue model is at risk. Boeing is a rare case where a structural moat (duopoly) is being rendered useless by total operational failure.

Airlines like United and Delta have been focused on retraining pilots to use newer airplanes like the Airbus A321neo because the cost of retraining is cheaper than waiting 5 years for a Boeing plane that might get delayed again.

R&D spending might be high, but the return on capital is weak – R&D isn’t making their profit or FCF go up.

Their customers hate them. The constant problems that are incurred around their defence division are not small either: in 2024, they incurred $5 billion of additional losses from their fixed-price development programmes (a contract which doesn’t change in price).

This is very similar to what happened to Rolls-Royce in 1971 – they were also overburdened by fixed-price contracts, and the UK government decided that their failure would be a threat to national security, so they nationalised the company. The shareholders were left with nothing. After reprivatisation in 1987, they didn’t get anything.

In the same year, we had the Lockheed L-1011 TriStar jet development. They started running out of cash because Rolls-Royce effectively went into bankruptcy and could not get their engines, thus not being able to deliver planes. The company survived, but it had to be overseen by the US government – it was not able to take any risks and thus limited its growth. The stock price took a decade to recover.

You can see the weak capital return – the company is effectively in the same situation as the two companies I talked about – a “zombie” state - it’s only a matter of time in my view that they will have a big issue. I think that if Boeing fails, the government will take equity instead, leaving investors with scraps of a diluted company.

Quality Score analysis dashboard showing a moderate 4.9 out of 10 score.")

Boeing has a Nabzdyk Ratings quality score of 4.9/10. We can still see the same issues as before: weak profitability and high leverage, but their operations are improving in terms of efficiency. They are reinvesting their cash in a way that is better than before – although they still have weak profitability – so they are clearly aware of the situation and will continue doing this. The elite rating in asset efficiency is a huge red flag, actually – and that’s because of their weak profitability. They are using their assets to the maximum, but not getting any further in terms of profits – what shareholders care about. The aggressive leverage doesn’t help here.

I never had the intention of owning this company, but if I had to, I would rate it as a SELL because, contrary to what some people may claim, it is not undervalued. I see it as a potential bailout that will wipe out its shareholders.

Boeing manufactures planes. It also creates defence machines for use by the military. They also produce satellites. But recently, they have declared that they are scared of companies like Palantir, SpaceX and Anduril (not directly, but it literally says so in their 10-K):

In 2024, they didn’t mention that risk. Now they do; they are clearly capable of predicting what can be next.

They have three segments:

• Commercial Aeroplanes (BCA);

• Defense, Space & Security (BDS);

• Global Services (BGS).

Global Services Segment

This provides their customers with services – maintenance, modifications, upgrades, analytics and others. The most predictable driver of revenue.

Why do I say predictable? Because its costs are rather fixed – meanwhile, the products are getting more and more expensive – this doesn't help because their customers are ultimately their hostages – they can’t pick a different provider because their competitor Airbus might be fully booked. So while they might have a duopoly, it’s built on sand, not stone.

Another aspect is the trend of it – in 2024, their product sales decreased, while services increased.

Commercial Airplanes

They develop, manufacture, and sell the 737 narrow-body model and the 767, 777 and 787 widebody models.

Defence Space & Security Segment

Research & development of manned and unmanned aircraft and defence systems.

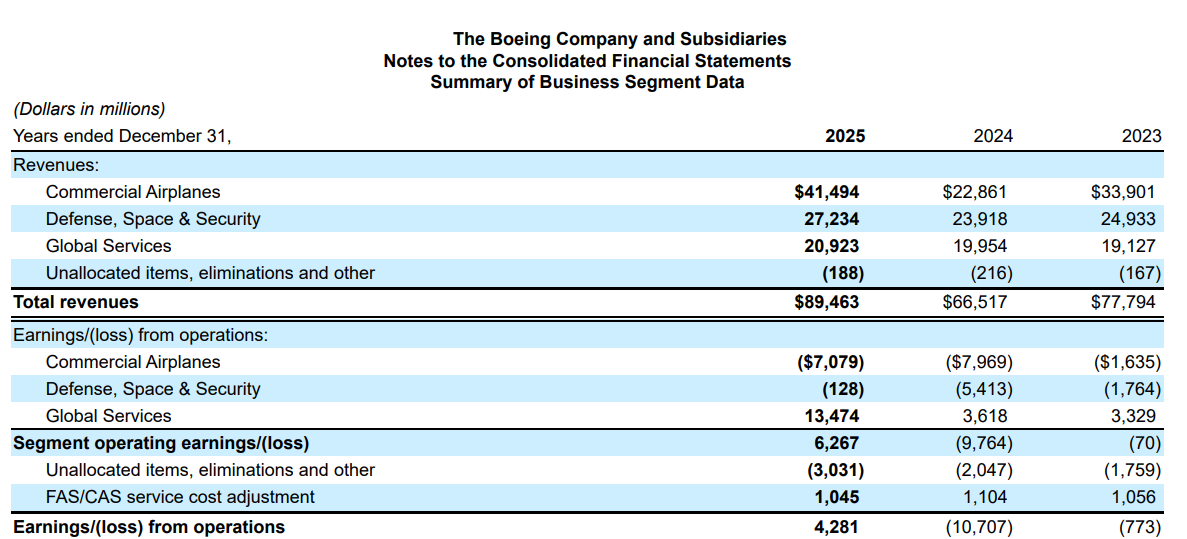

As you can see, margins are low, and their financial health shows a bleak picture: too much debt.

balance sheet health showing a negative net equity of -$28.8B and a negative net cash position.")

This is a terrible asset situation.

37% of their workforce is unionised – a major risk if something like workers’ pay increases isn’t there; this can drive a company’s profitability significantly down, or impair their asset base even further.

model. The initial estimates are listed: their revenue growth, and an 8% discount rate.")

We can’t perform a valuation on a company with negative FCF.

Antoni Nabzdyk

This isn’t financial advice.