Coursera

A moat contender - earn a university degree without the hassle of going there.

. It features the Coursera logo and the title 'A story of education', focusing on the online learning platform.\"")

Industry: Services-Prepackaged Software - CAPITAL_LIGHT archetype

showing a Good score of 5.9 out of 10. The analysis highlights 'Elite' Financial Lock-In and Workflow Integration, but 'Weak' Product Lock-In due to growth efficiency issues.")

Coursera scores a 5.9/10 in the NabzdykRatings Moat Score.

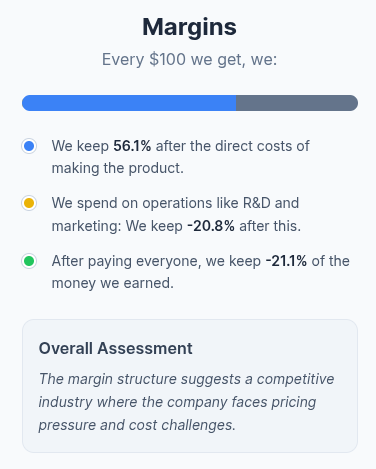

The workflow integration of their offering is strong: they are used by students to learn something new, so once you join, it’s unlikely you’ll stop paying in the middle, and also, you may start another course, being financially locked as a result. However, the score is moderated by weak growth efficiency: their most recent earnings report suggests they are generating less cash per dollar of revenue.

Companies which join Coursera’s courses will likely stay. Why?

It’s not because of the self-hosting of courses that would be necessary otherwise; Google has that – it’s rather because of the target audience that Coursera offers – it’s large, 183M+ to be exact. This is a financial lock-in – moving away wouldn’t be smart financially for them, as it costs nothing to join Coursera as an education partner.

showing a Weak score of 4.4 out of 10. The report indicates 'Good' Operational Excellence but 'Weak' Asset Productivity and Cash Efficiency.")

Coursera scores a 4.4/10 in the Nabzdyk Ratings quality score.

As I said before, efficient growth is crucial for a business in the capital-light archetype. Coursera isn’t one of those companies – while they are returning capital to investors in a good way, they don’t put their assets to a good use: with their recent acquisition of Udemy, their cash had a drag, and they are yet to turn a GAAP profit.

Coursera collaborates with universities and companies – they make it possible to earn certificates for a job, e.g., a bachelor’s or a specific course designed by Adobe, Microsoft, Google or others. The courses developed by these companies are made to align with certain positions at those companies, making Coursera sort of a “discovery” engine for companies seeking talent in different ways.

Their collaboration with ECTS, ACE and NSQF means they are focused on being recognised as a platform that has education that matters to employers.

Coursera is different from Udemy or Duolingo, with a focus on entry-level professional certificates, because they believe that as more jobs become automated, people will look to level up in their skill set away from the easily automated ones.

They offer professional certificates (more job-orientated) AND the more expensive ones for a bachelor’s degree.

But can’t a student just choose one and get a job anyway? Well, the professional certificate is what they need then, as it helps a person reach their job goals in months, not years.

On the other side we have the expensive courses I mentioned – those are essentially filters for uncompetitive candidates, as they are very fast-paced (around 8 weeks) and thus are more demanding than the traditional way of learning.

The company has recently pivoted to selling to CEOs of companies, which requires Coursera to ask for permission to showcase their ideas and negotiate contracts. All of that takes time and, in my view, is a distraction from their core business as they start to function as more of a “consulting” business instead of staying capital-light like they are supposed to be.

Selling to CEOs means that they are selling the idea of teaching the entire organisation because of the AI skills that employees should have – CEOs understand that and might be open to this.

I understand why they might view this as a better growth-orientated opportunity (being more stable in terms of revenue – a single customer cancelling a subscription is way more likely to do so than a 10,000-person company), but on the other hand, it’s an expensive process.

model.")

. The Reverse DCF shows the market is pricing in a negative growth rate of -32.0%, suggesting the stock is priced for distress or bankruptcy.\"")

I don’t want to buy this company, but investors who are comfortable with taking on some additional potential volatility in revenue can buy this company, as the current price of $5.83 implies a FCF growth of negative 32% for the next 10 years – effectively, the market is pricing this company for an unlikely bankruptcy. For these investors, it’s a BUY.

For my personal portfolio, it’s a SELL, as I don’t feel comfortable holding this company, as it’s in a transition phase.

The company is in an uncertain position – not something that I want to have, except for when I understand a company fully (such as Duolingo). Investors should take into account the expenses that Coursera might make in the near future. Their balanced NabzdykRatings Moat score represents the uncertainty of the market towards their uncertain future.