FirstSolar – updated methodology

An asset-heavy commodity - Innovator archetype - v1.2

deep dive analysis cover image. Title: 'A story of solar panels.' Identifying the investment thesis for a leading solar manufacturer.")

NabzdykRatings Moat Score analysis showing a rating of 6.3 out of 10 (Good). Key negative drivers include a Critical Sector Cyclicality Warning and Weak Structural Resilience. The analysis classifies FSLR as an Asset-Heavy Manufacturer.")

First Solar has a Nabzdyk Ratings Moat Score of 6.3/10 because the company is an asset-heavy manufacturer, which exposes it to high sector cyclicality. Notably, our quantitative model evaluates realised cash economics, rather than future promises (such as order backlog), ensuring we rate the business as it is today, not a future estimate.

NabzdykRatings Quality Score analysis showing a perfect rating of 10.0 out of 10 (Elite). Key positive drivers include Elite Owner Capital Stewardship, Strong Margin Expansion Profile, and Good Asset Expansion Discipline.")

First Solar has a Nabzdyk Ratings Quality score of 10/10 because of its strong margin expansion. Management has the discipline to refuse over-expanding its business, which creates value for shareholders, as evidenced by the “Good” rating on its asset expansion discipline.

The Nabzdyk Verdict:

This is not a buy-and-hold company; instead, it’s a company which requires investors to closely watch the macroeconomic cycle and backlog health.

Management is efficiently playing the cards that they have, but long-term investors must not treat it like MSFT or ADBE. Instead, investors should remain focused on the order backlog trend and the demand for solar panels in key geographies for FirstSolar, especially India & Chile, which are emerging markets where the most volatility is.

I rate this company a SELL, as it’s not a company that has a stable history - it’s a commodity player, which makes it even more unpredictable, and its recent turn to positive FCF doesn’t have to be a positive thing – it might be a temporary aspect – we don’t have enough history of their positive FCF (only a TTM period), so I won’t feel comfortable holding this company.

Methodology Update: Introducing the ‘Sceptical Gates’ (v1.2)

FirstSolar was selected for the series of “Hidden Champion” articles, and on paper, it was a solid pick - It’s even in the Nabzdyk US 20 index and has a high moat & quality score.

What can go wrong, right?

To fix this, we conducted a sector stress test on 14 key innovator stocks to validate the model:

The Darlings: NVDA, AVGO, ISRG, DXCM, RMD, MPWR, FSLR.

The Laggards: MRNA, IQV, HOLX, ON, REGN, TXN, VTRS.

In our pursuit of the Nabzdyk Standard, we constantly stress-test our models against reality. Our review of the ‘Innovator’ archetype revealed that V1.0 was too heavily weighted toward top-line growth. While appropriate for software, this created ‘False Positives’ for asset-heavy innovators like First Solar.

The Calibration:

We have upgraded the algorithm to v1.2. This update introduces stricter ‘Sceptical Gates’ regarding free cash flow conversion. Revenue growth is no longer enough; the algorithm now demands that growth contributes to cash flow per share.

The Impact:

To ensure absolute accuracy, we ran 7 top Innovator stocks, along with the bottom 7, through the new V1.2 algorithm, which now strictly penalises profitless scaling, capital erosion, and cyclical volatility. The recalibration exposed a massive divergence between market narrative (stock price) and structural quality (our score):

. Analysis of First Solar, NVIDIA, Broadcom, ResMed, and Intuitive Surgical. Highlights significant Quality Score downgrades for capital-intensive AI stocks like NVDA (4.4) and AVGO (3.6).")

First Solar manufactures solar panels, which, in their view, are innovative. While the product itself might be complex, it’s part of a larger commoditisation scheme around solar panels, where only price matters for the consumer. They are said to be “competitive”, but other than the long-lasting nature and their warranty on their product, they have a commodity: a solar panel.

Altough some might argue that their product differs than those of Chiense competitors, hcih primarily use Polysilicon.

A key aspect of this industry is demand. Electricity is always needed, and with the recent AI-driven data centre craziness, the power demand is going upwards.

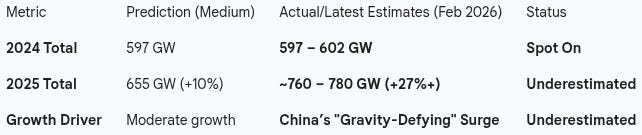

showing exponential growth to 597 GW. Highlights China's dominant market share compared to Europe and the Americas.")

This is exponential growth.

This 2025 prediction was an underestimate:

But this was driven by countries such as China, India, and emerging markets. Europe actually was left behind.

Net Sales by Geographic Region (2022-2024). Table highlights extreme revenue concentration in the United States ($3.9B) compared to volatility in emerging markets like India and Chile.")

Chile and India are emerging markets, while the US and France are more mature.

What happened that they finally had a positive TTM FCF number?

This is primarily because of the Inflation Reduction Act (IRA), which gives them credit for their parts.

But their strength lies not in the panels themselves but in the specific regulations around Chinese parts. China has forced labour. The US doesn't want that, so when big companies like MSFT or Amazon buy FSLR panels, they pay a premium for FSLR panels not for superior technology, but for Supply Chain Compliance and immunity from anti-circumvention tariffs targeting Chinese competitors.

That’s why they buy FSLR’s products – but for me, this feels way too temporary.

Key Quarterly Financial Data Q3 2025. Analysis highlights a divergence: Net Sales grew 80% Year-over-Year, but Gross Profit Margin compressed by 11.9 percentage points. R&D spending increased 21%.")

Investors are focused on the 80% revenue growth – unfortunately for us, the v1 algorithm also thought of that – but it turns out that’s NOT where the truth is.

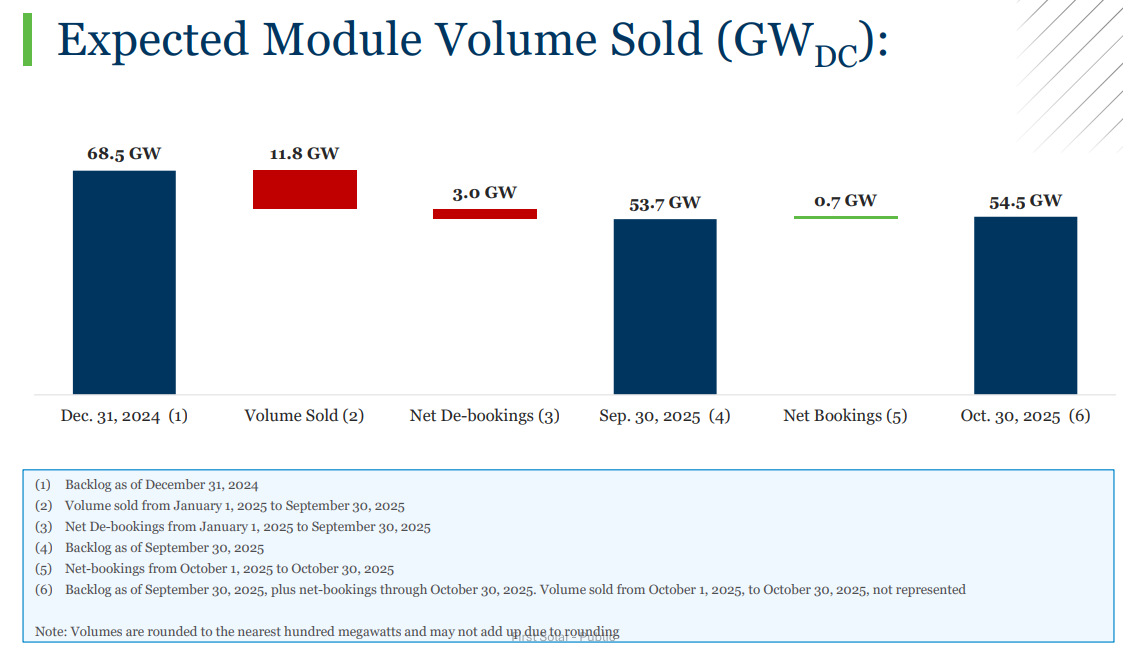

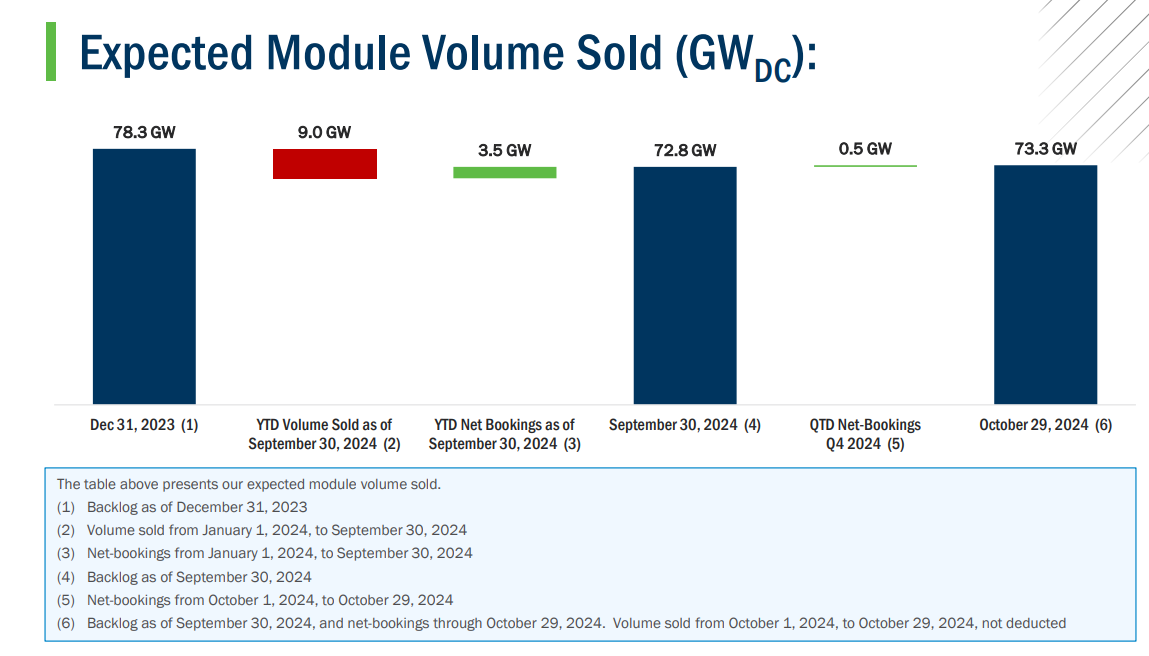

A key aspect of this business is backlog AND R&D efficiency.

This wasn’t anywhere to be found in their 10-K, which surprised me: why hide it?

I found it in some of their investor presentations:

Note the December 2024 backlog: 68.5 GW.

So, year over year, we have a decline of the following:

formula: new old/new new = -14.3%

(Note this is 2023 vs 2024.) We don’t have their full 2025 data – we'll see the details on the 24th of February. I predict they will fail in terms of their backlog.

This means that some of the companies in my index shouldn't be there, but I will wait until the rebalance – I’m NOT going to modify the index manually; it’s meant to be recalibrated by an automated system, not a human.

Their business is in a pricing war – the solar farm owners typically want to have as low of costs associated with the production of energy as possible – they will probably pick cheaper Chinese panels, although with the recent Trump administration tariffs, it’s hard to say what they will do. FirstSolar makes some of their panels in the US, and that makes the whole situation far more complex.

The revenue growth of this company is very high: 31% as of the most recent quarter – year-over-year growth on a TTM basis.

financial analysis showing 31% Year-over-Year Revenue Growth contrasted with a commodity-style margin profile. Visualizing the disconnect between top-line expansion and operational value capture.")

But looking only at that is one of the worst things an investor can do – investors need to look at the free cash flow, which is what matters in valuation.

model.")

Reverse DCF Valuation Model by NabzdykRatings. Calculation shows a Market Implied Growth rate of 22.6%. The verdict is 'Attractive' (Undervalued) relative to historical turnaround potential.")

FSLR is a turnaround story: you can see that their FCF effectively went from negative to positive, so whether it’s truly undervalued is tricky; the valuation of a turnaround is always more risky than the valuation of a stable one.

I find it really interesting how you use "Sceptical Gates" to look past the high quality scores and address the volatility of a commodity player like First Solar. Do you think the recent shift to positive FCF is just a lucky peak in the cycle, or could their backlog discipline actually be a sign that they’re finally breaking away from the typical "boom and bust" nature of the solar sector? :)

I’ve subscribed and would be happy to support each other. We might not be in the exact same field, but I really like your analytical style—maybe you’ll find my content interesting too!

Jorrit