Nu bank.

Swoosh. You enter the first bank you saw while traversing the streets of Columbia, while on your vacation. You were surprised at the lack of bureaucracy visible at the bank. Customers seemed happy while leaving the bank. You also took notice of the wide variety of people in there. This bank crossed all the barriers which were made by other financial institutions. The freedom to open a bank account for many people. While you sit there and wonder, your gaze falls upon the logo of the bank “Nu bank”. Now back to reality. Is this bank truly a spectacular investment, like many people think? Let’s check it out! :)

Stock Information

Buying a stock without knowing what it does is like running into a dynamite factory with a lit match. There’s bound to be a BOOM! But we are investors that don’t take emotional decisons, for that, let’s look at what makes this bank different.

Large customer base - 114 million customers in the emerging markets? I mean, that’s pretty strong growth, isn’t it?

No Fees or Lower Fees - NuBank went the opposite direction that many traditional banks, by making their products have a low or no fee.

Customer-Centric Approach - Resolving customer’s issues digitaly dramatically takes down costs, while seemlessly integrating with the user. Quick, via app/chat, compared to a customer support calline in traditional banks.

Strong Brand & Community Engagement - They are showing themselves as an alternative to the old banks, similar to how Revolut, Wise or Stripe operate. They are also changing the marketing startegy: around 80% of its new customers are acquired through word-of-mouth, which is the best method in existence.

What do they offer:

Credit Cards (NuCard or Ultravioleta, a premium card with 1% cashback invested automatically)

Digital Accounts - no fees with Instant and free transfers (PIX, TED, etc.), similar to the BLIK technology in Poland, my home country!

Personal Loans with a flexible ability to pay them off, with quick approval, all from their app.

Investments - Stocks, ETFs, government bonds, and fixed-income investments with No brokerage fees.

Insurance - Life and phone insurance with customizable plans, all from the app.

Business Account - ideal for freelancers and small business owners

International Services - credit card with no foreign transaction fees.

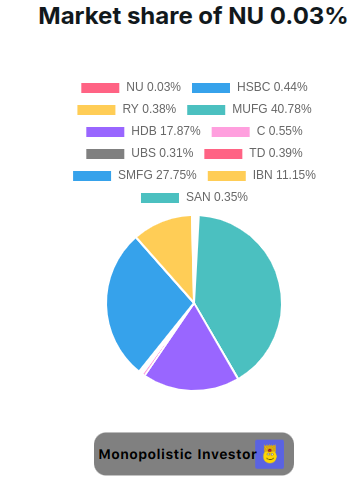

That’s what they do. What’s even more interesting, is that their monthly average customer cost sits at around $0.90! Absolutely unthinkable! Let’s take a look at their market share, to see whether they are a monopolist, or not! :)

This has been generated using my own tool, that I personally developed:

We can see that NU has a very, very small market share, almost insignificant to other companies, but we must also look at their growth trajectory, which has been absolutely mind-blowing over the past few years:

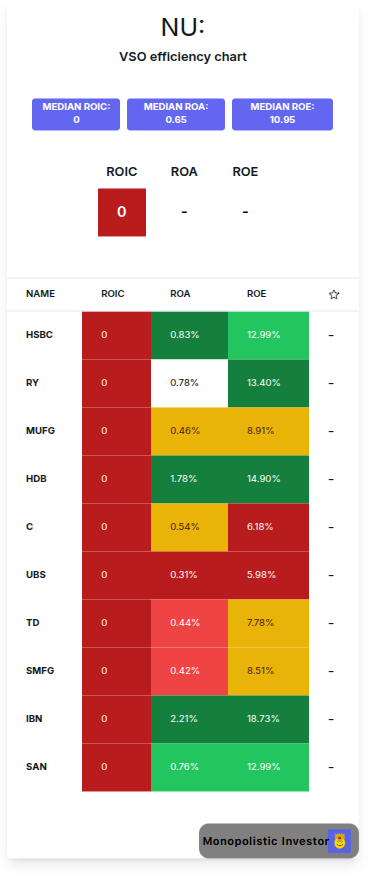

Ok, so we got to know what this company does, how does it stack up against their competitors, apart from the market share? Financial efficiency, that’s what. Here’s a VSO (Versus others) chart I developed myself:

Unfortunately, due to the nature of the banks, don’t give too much attention to ROIC. Here are other metrics we need to take a look at:

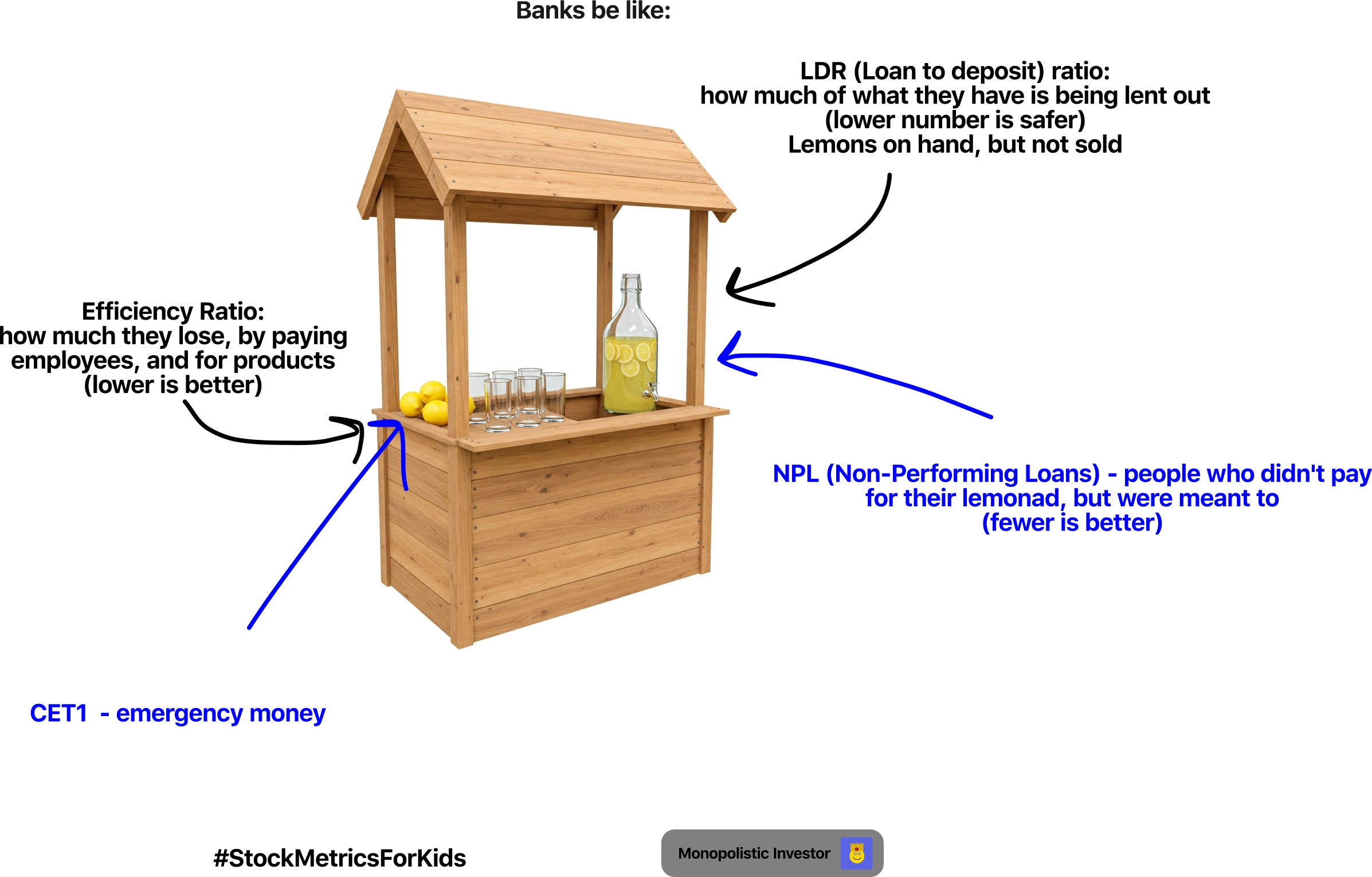

We will use a lemonade stand analogy:

NIM (Lemonade Profit %) – Net Interest Margin: How much profit per dollar lent, or the difference between how much they give loans for (22%) and the interest on accounts (5%) is equal to 17.7%

Efficiency Ratio (Wasted Lemons %) – Lower is better. As in, you spend $100 for lemons, but employees take $30. - that’s an efficiency ratio of 30%, and the lower it is, the better. That’s NuBank’s ratio: 30%

LDR (Lemonade Sold %) – Loan-to-Deposit Ratio, or How much they lend vs. hold. You have lemons on hand, which you can use, but you didn’t, instead keeping them as a backup. NuBanks ratio is 40%.

CET1 (Emergency Lemons) – Common Equity Tier 1 or Backup money for safety. If your lemonade stand starts to lose money, you need to have a backup - Nubank has way more than the required minimum, meaning it’s very safe and strong.

NPL (People Who Didn’t Pay for Lemonade) – Non-Performing Loans. Fewer is better. If you give 100 people lemonade on credit but 4 of them don’t pay within 3 months, those are "non-paying customers" (NPL). Only 4.1% of loans are overdue (15-90 days), while 7% are seriously overdue (90+ days), but this was expected.

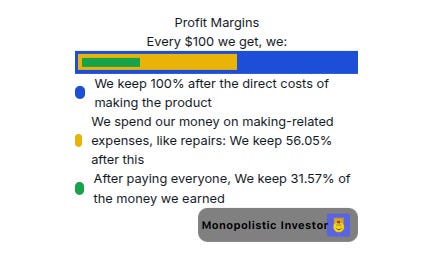

I think you understand it now, don’t you? :) Now, let’s look at the percentage of money they make from revenues:

We can see that they make 31.57% of their mmoney. That’s high for a financial instition, but not the highest, but we do see room for margin expansion.

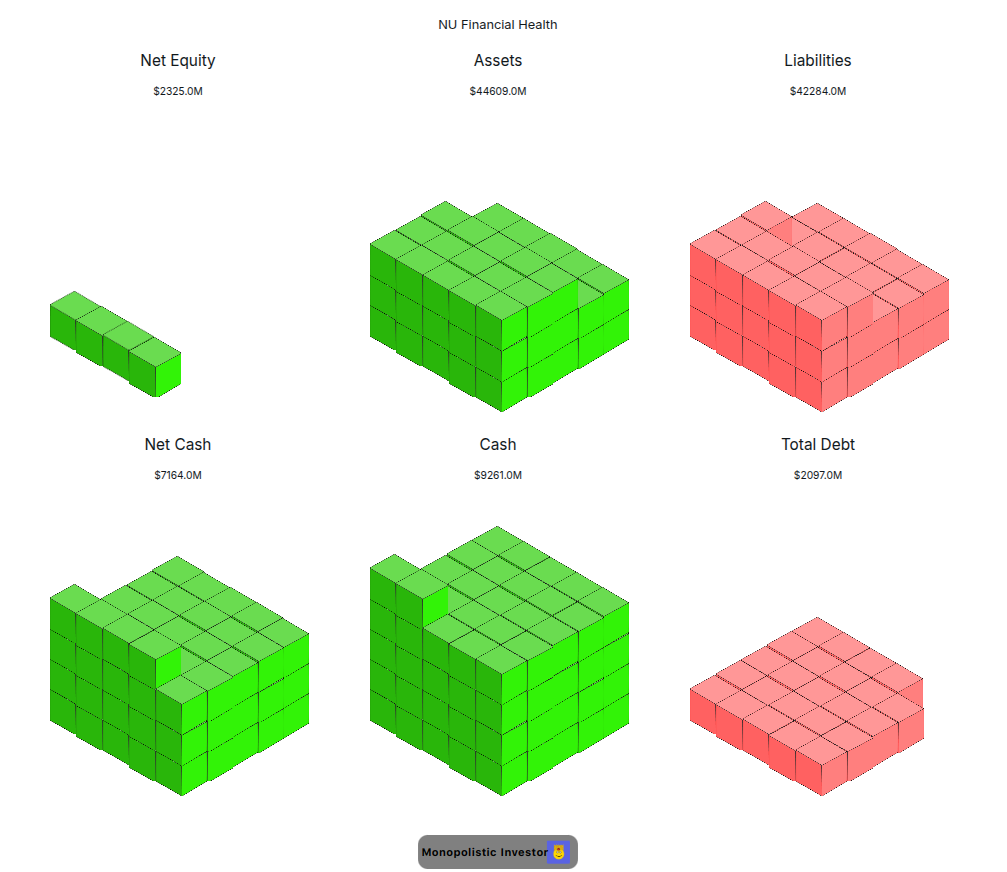

Financial health

Anytone who doesn’t check the financial health of a company before investing is an ignorant person. They aren’t even investing. They are gambling. That’s why I have created a transaprent overview of whether a company is in a great or terrible financial situation. Here it is (developed by me, you won’t find it anywhere else):

We can see a really healthy company, with a net equity AS WELL as a net cash position, which is especially important for banks guys!

Debt / Equity is at only 0.27! 0.27 years! That’s incredible!

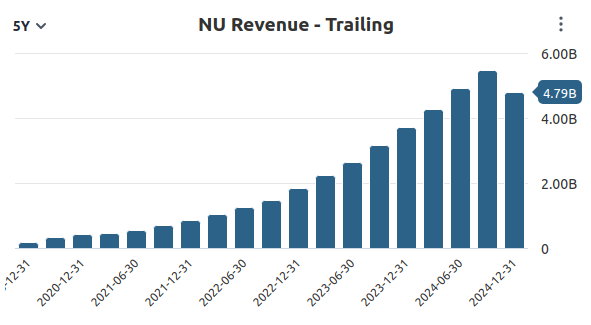

Revenue growth

We want fast-growing companies, not stalwarts (except for 1-3 stocks, that is, like MDLZ, MO or other). Does it have that?

We can see a company with almost exponential growth for its past, but does it mean that this will continue forever? I don’t know, but they are profitable right now, so that is the most important thing, right? :)

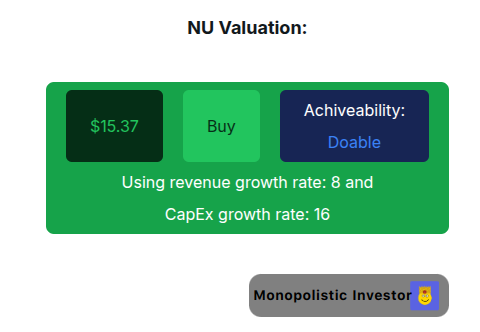

Valuation

We don’t want to overpay fro groceries, so we will go to discount stores. We don’t want to overpay for stocks - we buy them at lofty valuations - Random retail investors. I see this time and time again. The smae, smae old story, where the investors overpay for a company by a wide margin, and lose money in the process. We don’t do that here.

We take a patient approach, as even a high quality company can be devastating for us, if bought at a price level not great for us.

Here’s NuBank’s valuation, using a tool that I made myself:

Conslusion

While I do see Nu Bank’s potential, I made a decison not to own banks, as they have liabilities in the form of unpaid loans, and I want predictable companies. While that doesn’t mean I’m bearish on the company, I myself wouldn’t be comfortable owning this company. Any new investors in this stock will be greatly reqrded in my opinion, but it’s not for me! :)

Do you have any questions, or suggestions? Why not leave them in the comments below or a quick 2-minute survey?

Here’s a short bonus for the premium subscribers (join for a 30-day free trail, no commitments, cancel anytime) - a short video showing the timeline of the future financial health of NU: