Oracle.

Bzzzz. The humming of the computers in the cold server room, let you know you’re in a different place. A giant library for all businesses alike, allowing them to access data at 60 GB/s. It’s certainly an intruiging place to be. But is this a great investment? Let’s find out! Also, this article is made in part by my friend, dividendsjourney :)

Stock Information

But what do they even do? Easy, they organize the data that businesses use, handle tasks like accounting, human resources, and customer relationship management. And of course the cloud. The market share is almost non-esistent, though, sitting at just 6.8%.

Stock Revenue

Q1 2025 Earnings

Key drivers for growth were Oracle’s cloud services. Cloud revenue (IaaS + SaaS) totaled $5.6 billion, up 21%. Cloud infrastructure revenue showed strong demand, growing by 45% to $2.2 billion. Cloud application (SaaS) revenue was $3.5 billion, up 10%. Cloud ERP systems, including Fusion and NetSuite, brought in $0.9 billion each, up 16% and 20%, respectively.

Q2 2025 Guidance

Safra Catz, CEO of Oracle, expects strong demand for its cloud and ERP services to continue in the next quarter. The company anticipates further 8-10% revenue growth, with earnings per share projected between $1.45 - $1.49.

Financial Health

We Investors want to buy healthy companies. But is this company healthy?

Debt to EBITDA sitting at 3.67. Google has less though.

Valuation

Oracle’s price-to-earnings (P/E) ratio is 44.960, compared to MSFT at 36.037 and IBM at 23.241, making ORCL more expensive than its main competitors, which is surprsing, as they don’t have a vast market share. But what is even more surprising is that Google, the world’s most used search engine, has a P/E of 22.259. What?! Seriously, a better opportunity there.

Profit margin

20.40% Profit margin isn’t bad, although it could have been better. Look at Visa.

Dividends

Oracle is a dividend player. It is dividend yield is 1,02%. The companies has 10 years of dividend growth and 5,26% dividend growth per year. ORCL’s payout ratio is 41,23% which make the ORCL shares a safe dividend play, albeit a slow growing one. :(

Conclusion

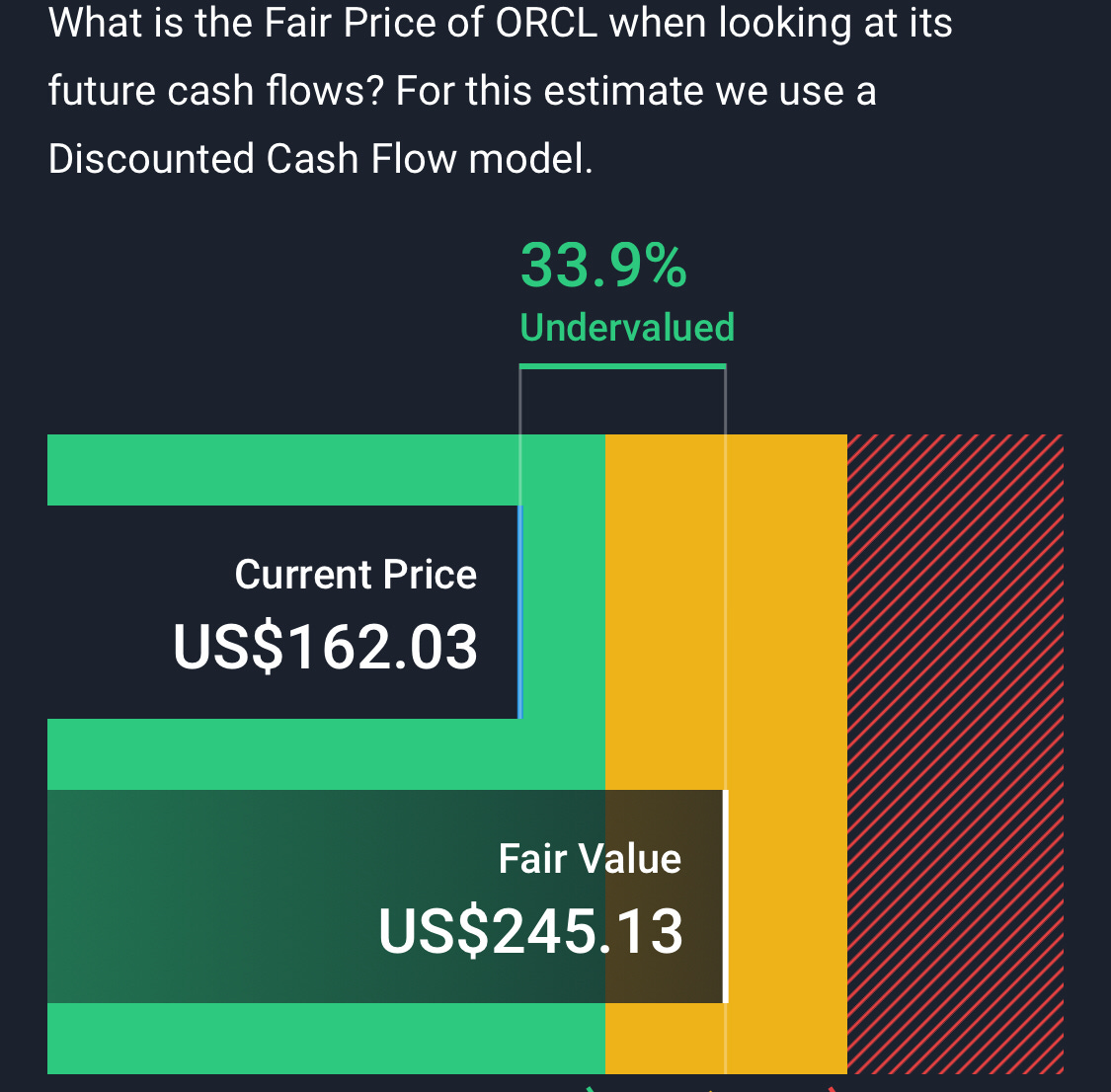

We do not see much more opportunity for growth here. Oracle’s shares are trading at a bigger premium than even Microsoft, which I don’t think they deserve. We see much more opportunity for growth in Google. A company that has a wider moat at a cheaper price is exactly what I’m looking for. ORCL shares are trading shy of it is all-time high ($160.52) $157.18 after the 13% shares pop-up on Monday post earnings call.

By: dividendsjourney & me

PS. I recently started a youtube channel with funny investing videos: https://youtube.com/@monopolisticinvestor?si=FFWIK4b8ZgjebNQW Check it out! 😀

| A guest post by

|

Oracle's performance in Q4 2024 and Q1 2025 is poised for continued success, as evidenced by the company's recent earnings and strategic developments. Here's an analysis of the current indicators and market trends:Strong Q1 Performance: Oracle's Q1 FY2025 earnings exceeded expectations, with a 7% year-over-year revenue growth to $13.3 billion and a 17% increase in earnings per share to $1.39123. The cloud infrastructure business saw a significant surge, indicating strong demand for Oracle's cloud services.Cloud Growth Momentum: The company's cloud services are a key driver of growth, with cloud services and license support revenue increasing by 10% year-over-year to $10.519 billion3. Oracle's cloud infrastructure revenue grew by 45% year-over-year to $2.2 billion, reflecting the company's success in providing cloud infrastructure for AI workloads.Strategic Partnerships: Oracle's partnership with Amazon Web Services (AWS) is expected to further enhance its cloud capabilities and market share13. This partnership brings Oracle's database services to Amazon Web Services through Oracle Database@AWS, opening up new opportunities for growth.AI Innovation: Oracle has announced new AI capabilities within its Oracle Fusion Cloud Applications Suite, including over 50 new generative AI agents4. This innovation is likely to attract more customers and contribute to Oracle's position as a foundational player in AI.Financial Projections: Analysts have revised their EPS forecast 13 times to the upside and 5 times to the downside in the last 90 days, indicating a generally positive outlook5. Oracle's total sales are projected to increase 9% in fiscal year 2025 to $57.82 billion1.Market Positioning: Oracle's cloud services are essential for companies like OpenAI, AWS, and Google Cloud, highlighting its foundational role in AI development6. This positions Oracle as a critical player in the AI ecosystem, with potential for increased revenue from AI-related projects.Stock Performance and Analyst Ratings: Oracle's stock has surged following the earnings report, and analysts have raised their price targets, suggesting a potential upside7. DA Davidson has lifted its price target to $140.00, indicating confidence in Oracle's future performance.In conclusion, Oracle's strong Q1 performance, strategic partnerships, and AI innovation position the company for continued growth in Q4 2024 and Q1 2025. The company's cloud services and AI capabilities are increasingly in demand, supporting a bullish outlook for Oracle's stock performance.

Very good review!