QSR.

Swoosh! The automatic doors open, leading the way to a tasty-smelling interior, where delicious food is being made. Burger King. Your favourite restaurant. You look across the street. You see a Popeye’s. You wonder: Just who is this company owned by? The answer: Restaurant Brands International. But is it really a good investment, or just an old company deemed to obscurity? Let’s find out! :)

Stock Information

| Seeking Alpha")

QSR owns a few restaurant chains, including Burger King, Popeye’s and Time Hortons, which are world-recognised brands. They own 31,525 restaurants, and operate in more than 120 countries and territories. They offer a wide variety of food in the format of a quick prepared meals, hence the name QSR (quick service restaurant).

We franchise and operate quick service restaurants serving premium coffee and other beverage and food products.

QSR earnings report

Here’s their market share (made using my tool):

Their market share is (taking away the HTHT, as it’s a hotel chain in China - my tool sometimes gets their competitors wrong, but I’ll fix it!), quite a bit, although it’s behind yum and ARMK (A catering provider in the US), so not the worst, but also not the best, my opinion: MEH.

Next up, let’s look at the efficiency of the company (how much cash invested yields good returns), (as we want our companies to be like a steam train that goes at max speed, right?):

VSO financial efficiency chart (also made using my tool):

We can see that QSR looks quite well against its competitors. The only companies rthat might be of some worry right now would be WING, RRR and WH. Maybe you’ll check them out next?

Let’s now move on to the profit margins, as we want them to be as high as possible, in order to maximise returns.

The ending profit margins aren’t the best, but I mean, for a restaurant, they are still ok. What worries me more is the gross and operating margins being a little bit too low for my liking (upwards of 50% is a must, if the company doesn’t have a monopolistic position).

Financial Health

The financial health cubes, which you are going to see in a moment are made out of 125 blocks, each cube being proportionally divided, and some hidden, so that it reflects the real proportions between the values, red mean negative values, and green positive. AND they have been made using my own tool:

We can see that QSR has a terrible minus net cash position, meaning they have more debt than cash, making it a less stable of an investment. Meanwhile, their net equity provides them with some light of hope, like a lonely tank, in the midst of an ocean red of chaos on the battlefield.

Their Debt / EBITDA ratio (or how long they will theoretically pay off all their debt), is sitting at 6.4, meaning almost 7 years of debt repayments!

I don’t like that, my companies have debt to EBITDA’s AT MOST at 3. This is a major red flag for me. If you have any ideas on how to show complicated stock metrics easily, let me know, and I’ll try to create it! :]

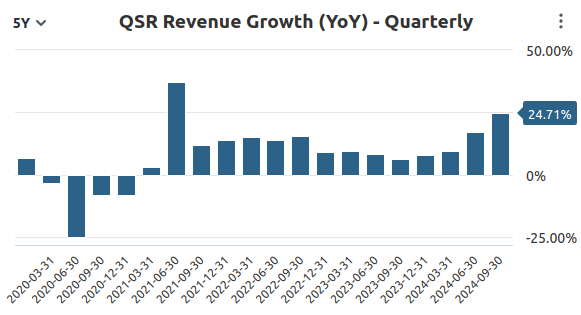

Revenue growth

We want our companies to sweep away the competition using their great pricing power, showcased by their strong revenue growth over time. Can QSR do it? Let’s check!

What these three charts show us (from stockanalysis.com), is that we have here a stagnant monster here. It’s not a monopolistic monster, but a stagnant one. So a sad thing for us investors!

Why it’s a Stagnant Stalwart? Well, beacuse even if we factor in their revenue growth, look at their net income, it’s staying in one place, while their operating expenses (which can be used for growth), are also not that big:

I’d rather they went up a little bit more, so they can grow better, but they aren’t, showing us a picture of a slow-grower.

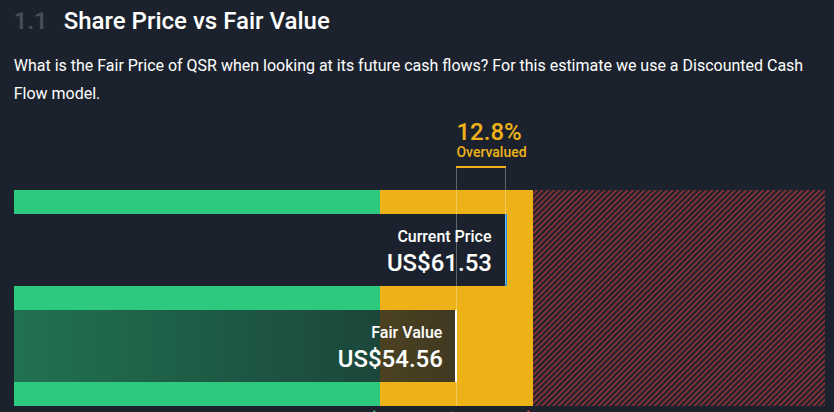

Valuation

Ok, so we have a slow-grower here, but even so, is it a buy, versus its current price of $61.82? Let’s see, and use my awesome tool that I use to estimate valuations for companies:

And now simplywall.st’s:

Conclusion

As you can see, we came to different conculsions, but for me, this stock isn’t a buy, given their small market share, and their overall stagnant nature of the business. Food companies are by no means a necessity, as we always will need to eat, but I think that a company like MDLZ is a better buy right now, given that they own many brands internationally, and they offer snacks all around the world and aren’t constrained by phisical locations, only factories.

For me, QSR is a hold, but if you buy it, you just bought a slow growing company.

great write up

McDonald's is racist.