Value Line.

shuffsf. The rustling of paper next door makes you get up. You work in an investment company, and paper is rare in your high-tech office. Your friend is looking at an extensive piece of a document a nd he turns around and says, They have finally come in, and they were right”. You come closer. It’s a financial report from ValueLine. You look at it again. It’s detailed. But then a thought crosses your head, “But are they investable?”. Let’s find out! 🙂 Today we’ll be taking a look at Value Line, together withFelix, who also owns an investing newsletter that focuses on value companies. The first part will be mine, and he’s will be after that!

For this analysis, we’ll have our friend Market Mike guide us through that analysis:

Value Line is in the business of making investment newsletters, much like we do here on Substack. Except they do it on a much bigger scale, having both digital versions and paper versions. They offer monthly, weekly and daily newsletters. Each of them is targeted at different types of investors who prefer different forms of reading. They also allow their users to research companies for themselves, like through their stock screener, and other functions.

A seasonality in their business hasn’t been noticed, mainly because their readers mostly use the annual option to pay for their articles.

Pro Equity Research is the tool that offers users the ability to look up to 3 years of historical data and reports of around 90% of all US stocks. Some of their more advanced versions offer advanced charting options, vast databases of companies' reports, and more. All in one place. This is a more detailed overview of their products:

The Value Line Investment Survey® —It is a digital and printed version of their publication, which provides its subscribers with actual unbiased equity research by only having the analysts who don’t own the specific equity analyse it. Each stock is reviewed quarterly unless some significant events take place in between quarters, in which case, their team of analysts creates an additional Supplementary Report. Their newsletter provides insights into companies from over 100 industries, proving a vast amount of knowledge all in one place. It’s a weekly subscription.

The Value Line 600 - a monthly service offering a similar set of features as the Investment Survey, but offers more in-depth research on the more dominant companies, around 600 included from the Value Line Investment Survey. Offered in printed and digital versions.

Value Line Select® - Value Line selects one stock every month from its ValueLine 600 selection of stocks that they think will achieve the best returns overall. It’s offered in both digital and printed versions.

They own many more publications, and for those of you who want to see them all, you can check out their 10_k for more information, as I don’t see much difference whether I explain them to you or not.

If we take a look at their profit margins, we can see a company that is well managed.

As they have paid everyone, they keep 60% of everything. My chart went haywire here, as it seems almost illogical for their operating margin to be only 16%. The possibility is that they receive a significant portion of their profit from things like interest payments from their cash, or Interests in EAM Trust are gain: they mentioned the fact in their annual 10-K report that they hold major stakes in the EULAV Asset Management Trust (EAM), which is an adviser to the Vlaue Line Mutual Funds. Because of that, ValueLine gets paid a small portion of EAM revenues. Clever! ValueLine also owns investments in stocks (dividends) or ETFs, and a dividend payment is included here. If you don’t know how operating and profit margins work, look here:

The competition in the space of financial publications is fierce, with the rise of Substack, and tge many small newsletters, as wwll as the more established players, which include (Value Line 10-K report): Daily Journal Corp, Forrester Research Inc., Donnelley Financial Solutions, Marketaxess Holdings, Moody’s and Morningstar.

Their competitors (Moody’s and Morningstar) are worldwide recognised standards of rating. While Moody’s is in the business of credit rating, Morningstar is a lot more similar in its targeted research towards certain companies. Many of the things they offer are free, but they have also expanded their reach in terms of independent research: they give users a lot of data on thousands of stocks in simple ways. That’s similar to what I’m trying to achieve.

The Daily Journal Corporation is in many ways similar to Value Line, offering publications and news regularly, but not in stocks, but in real estate and legal stuff, mainly in California. They also offer a software (much like Morningstar and Value Line, but for case management for courts and governments, unlike others), and were even chaired by Charlie Munger at one point.

Forrester Research provides business reports to make it easier for those companies to evaluate their future, market behaviour and technology trends. This is high-value knowledge and thus provides pricing power for them.

Donnelly Financial Services provides products in the compliance and risk sector, making it easier for companies to make reports like the annual or quarterly ones, as well as communication.

MarketAxess is an online platform for trading of corporate bonds and other fixed-income securities, like certificates of deposit, but I don’t see why they have included them as a competitor, as they serve different segments of the broader financial industry.

Here is a market share chart I developed (from Excel), and here is the one generated by my tool:

MarketVision:

Similar companies, similar percentages, but different. You can check out my tool, as always, for 30 days free with your Substack paid subscription.

When we compare their competitors to them in terms of financial efficiency, we see a clearer picture:

, ROA (5.05), and ROE (15.45). Below these medians, a section shows current ROIC at 4.21% (red), ROA at 2.99% (red), and ROE at 22.87% (green). The main part of the chart is a table comparing various companies (SSTK, SCHL, DJCO, MKTW, TRI, MORN, NYT, BRDG, VRTS, AAMI) across ROIC, ROA, and ROE metrics, using a heatmap-like color coding (green for good, yellow for moderate, red for low performance). Some rows have a star icon on the right, indicating a notable performance. A \"Monopolistic Investor\" logo is at the bottom right.")

Morningstar beat them as well as AAMI (No idea what that is) - I analysed Morningstar before, let me just say that it was an interesting company, but not with a wide enough moat. 🙁

So maybe AAMI is better?

Their financial health is as follows:

, Assets ($143.6M), and Liabilities ($44.6M), represented by stacks of green cubes for equity and assets, and red cubes for liabilities. The bottom row presents Net Cash ($71.9M), Cash ($75.8M), and Total Debt ($3.9M), also using green cubes for cash and red cubes for debt. A \"Monopolistic Investor\" logo is at the bottom center.")

We can see that they are a well-managed company, with more cash than debt, as well as positive net equity, which means they have more liabilities than assets! Shareholders are happy! 🙂

The green represents positive numbers, and red represents negative numbers.

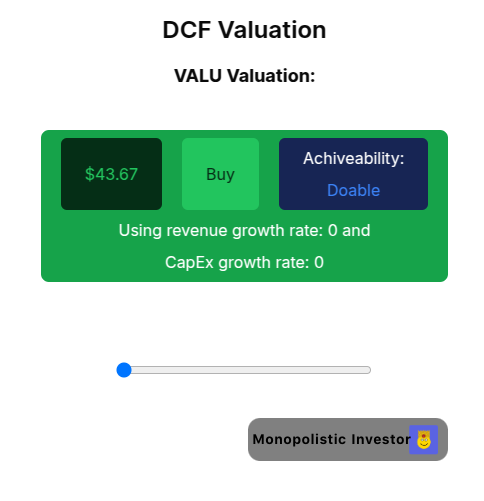

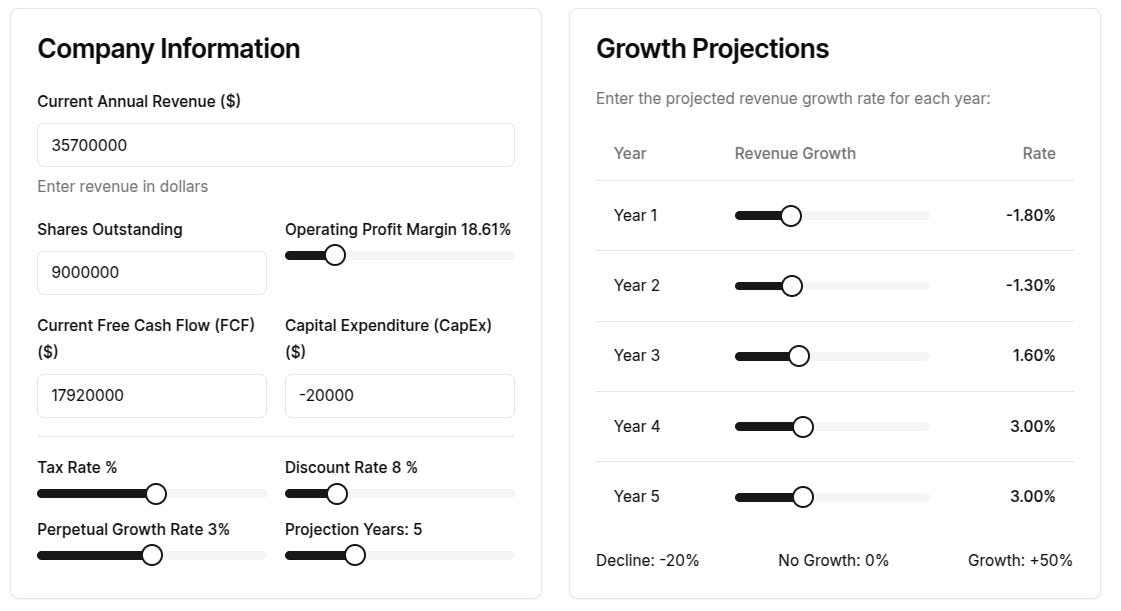

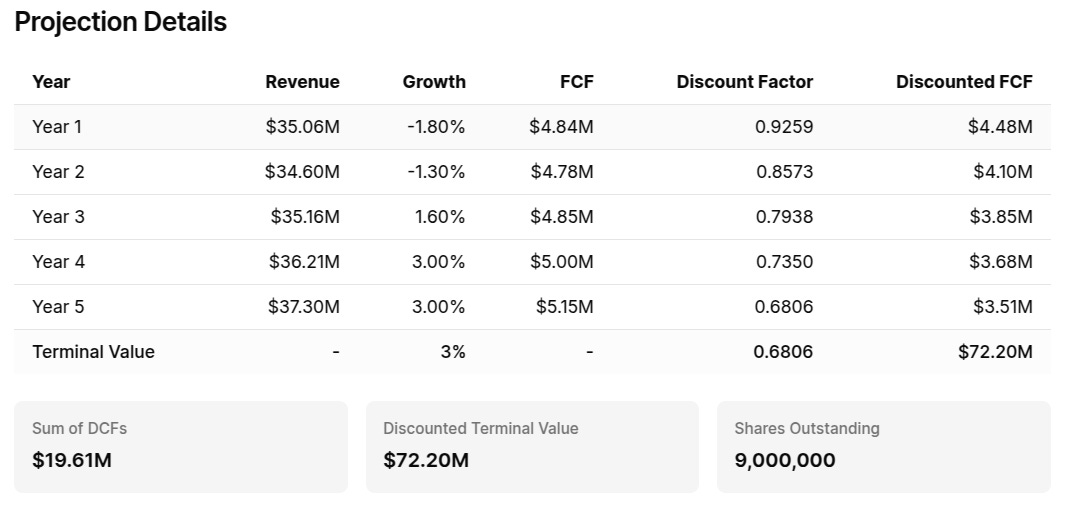

Fair value of ValueLine / What is the valuation of Value Line?

While I looked for any sort of outlook for ValueLine, there was none. Zero. So I had to make a calculated guess:

Scenarios are based on this chart:

I believe that 0% revenue growth is possible, I won’t forecast negative yte, but I think a 3% growth is possible, in line with the long-term inflation rate.

0% revenue growth:

3% revenue growth:

Here is a bit of a varied one (negative and after 2 years positive returns):

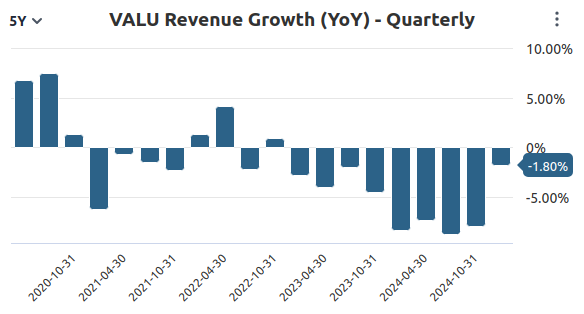

The third one is especially worrying. Although I don’t think they’ll go bankrupt, they need a revenue stream - and quickly.

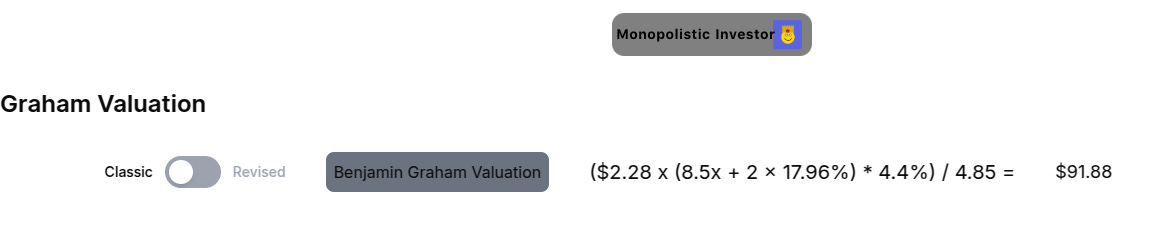

But that’s not all - we also have Benjamin Graham tell us a bit about this company:

* 4.4%) / 4.85 = $54.73. Above this, a gray box reads \"Monopolistic Investor\" with the number 5.")

While the first one offers more upside, I highly doubt whether that will happen, although we need to think, what if they do share buybacks? That’s how companies buy growth, similar to Apple, so it’s not like it’s a bad company, but a bad stock, with small returns.

Those valuations don’t offer much of a safety margin.

Memes I made on ValueLine:

Conclusion

While I see value in their investment periodicals, which were read by Warren Buffet himself, I think that the best thing to do now is to not buy this company, as for me, it’s a very small company with some clients (who might be defensive ones), but I’m not convinced of this company. For me, it’s a hold. For people who like that type of company, maybe a turnaround play, I think this is a good choice. This isn’t financial advice.

Felix’s part:

Stock Analysis: Value Line

Overview:

Business Model

How does Value Line make money

Do they have a Moat?

Products/Services

Future Outlook

Conclusion

Value Line, Inc. (NASDAQ: VALU) stands as a pillar in the investment research industry, delivering independent, data-driven analysis since its founding in 1931 by Arnold Bernhard in New York City. Renowned for its flagship Value Line Investment Survey, which covers approximately 1,700 stocks across over 90 industries, the company has built a legacy of trust and reliability. Catering to individual investors, financial advisors, and institutional clients, Value Line’s proprietary ranking systems and comprehensive datasets distinguish it in a competitive field.

This in-depth stock analysis explores Value Line’s business model, competitive advantages, financial performance, market position, and prospects, providing a holistic view of its investment potential in 2025.

Company history and evolution

Value Line’s journey began during the Great Depression, when Arnold Bernhard sought to create a standardised system for evaluating stocks. The Value Line Investment Survey, launched in 1935, became a cornerstone of investment research, offering detailed stock reports and proprietary rankings.

The company went public in 1983 under the ticker VALU and has since expanded its offerings while maintaining its core focus on independent analysis. Over nearly a century, Value Line has navigated market crises, from the 1987 crash to the 2008 financial crisis, by adhering to a conservative, data-driven approach. Its longevity underscores its adaptability and enduring relevance in the financial services sector.

e Line generates its revenue primarily through two business segments: Investment research and Investment management, as seen in the previous section.

Investment research revenue

The Investment research segment, accounting for approximately 70% of revenue ($30 million), is the backbone of Value Line’s income. This segment relies heavily on subscription-based models for its suite of research products, including the Value Line Investment Survey, Value Line Fund Advisor, and digital platforms like Value Line Pro. Subscriptions are sold on annual or multi-year contracts, with pricing ranging from $600 to $1,200 per year for individual investors, and higher-tier institutional packages exceeding $10,000 annually. The shift to digital subscriptions has been a key growth driver, with digital revenue increasing by 15% annually in recent years, offsetting declines in traditional print subscriptions as the industry moves online.

Investment management revenue

The Investment Management segment contributes the remaining 30% of revenue ($12 million), derived from management fees associated with the Value Line Funds. These mutual funds and investment vehicles charge fees based on assets under management (AUM), typically ranging from 0.5% to 1.0% annually. As of 2025, AUM for Value Line Funds is approximately $2.5 billion, generating stable fee income. Performance-based fees, though less common, may also apply when funds outperform benchmarks like the S&P 500, adding a potential upside to this stream.

Additional income sources

Value Line also earns modest revenue from licensing its proprietary data to third-party financial platforms and educational institutions, estimated at 2-3% of total revenue ($1-2 million). Additionally, the company benefits from low operational costs due to its lean staff of around 150 employees and minimal physical infrastructure, boosting its net margin of 42.9%. This efficient cost structure, combined with recurring subscription and management fee income, provides a stable and predictable revenue base, though growth is limited by its niche market focus.

Do they have a Moat?

Value Line’s competitive advantages, or economic moat, ensure its resilience in the investment research industry. These include:

Proprietary ranking systems

Value Line’s Timeliness™ and Safety™ ranking systems are its hallmark, evaluating stocks based on expected price performance and risk. Historical studies suggest that stocks ranked 1 for Timeliness have outperformed the S&P 500 by an average of 2-3% annually over the past 20 years, though past performance is not a guarantee of future results. This track record provides a unique edge over generic market analysis.

Brand trust and legacy

With nearly a century of operation, Value Line’s brand is synonymous with reliability. Its conservative, data-driven approach appeals to long-term investors, creating a barrier to entry for newer competitors. The company’s reputation is bolstered by its consistent delivery of high-quality research, earning it a loyal subscriber base.

Depth of historical data

Value Line’s datasets, spanning decades, enable in-depth trend analysis and sector comparisons. This historical context is invaluable for institutional clients and financial advisors, as few competitors can match the breadth and depth of Value Line’s archives.

High switching costs

Institutional clients who integrate Value Line’s data into their investment models face significant switching costs due to the time and resources required to adopt a new provider. This stickiness enhances customer retention, particularly among professional investors.

Independence

As an independent research firm, Value Line avoids conflicts of interest common among firms tied to banking or brokerage services. This impartiality strengthens its credibility, fostering long-term client trust.

Market position and competition

Value Line operates in a competitive investment research industry, facing larger players like Morningstar and S&P Global. Morningstar, with a market cap of $12.8 billion, dominates with broader coverage and a larger subscriber base. Value Line holds a niche market share, estimated at 5-10% of the investment research subscription market, focusing on its unique ranking systems and conservative approach.

Compared to Morningstar, Value Line’s coverage is narrower (1,700 stocks vs. thousands), but its proprietary rankings and historical data appeal to a dedicated audience. User reviews praise Value Line’s clarity and independence, though some note its higher subscription costs compared to free or low-cost alternatives. The rise of robo-advisors and free research platforms poses a challenge, but Value Line’s premium offerings target investors seeking differentiated insights.

Future Outlook

Value Line is poised for growth by leveraging its historical expertise in a digital-first world. The company has invested heavily in its online platforms, with digital subscriptions growing at 15% annually, reflecting strong demand among tech-savvy investors. Recent initiatives include an AI-powered stock screener and real-time market tracking tools, aimed at enhancing analytical capabilities.

The broader investment research industry is evolving, with trends like passive investing, robo-advisors, and AI-driven analytics reshaping the landscape. Value Line’s independence and deep datasets position it to capitalise on these trends, particularly if it can attract younger investors through user-friendly digital interfaces. However, challenges include intensifying competition and the need to maintain relevance in a market increasingly dominated by automated tools.

Potential risks include stagnant growth if digital adoption slows or if larger competitors encroach on its niche. Additionally, as a small-cap stock, Value Line may experience higher volatility, particularly in turbulent markets. On the upside, its strong balance sheet and sustainable dividend provide a buffer, while its digital transformation could unlock new revenue streams.

6. Conclusion

| A guest post by

|